New Delhi: The agriculture and allied activities sector have historically formed the backbone of the Indian economy, making substantial contributions to national income, employment generation, and rural livelihoods. With nearly 46.1 per cent of the population dependent on agriculture and allied activities for their sustenance, ensuring financial security and improved access to institutional credit for farmers remains a central policy priority for the Government. In this context, a set of targeted interventions has been introduced to strengthen agricultural finance, with particular emphasis on expanding and modernizing the Kisan Credit Card (KCC).The Revised Kisan Credit Card (2020) scheme seeks to ensure that farmers have access to adequate and timely credit for a wide range of agricultural requirements, including short-term crop cultivation, post-harvest operations, marketing-related expenses, household consumption needs, working capital for farm maintenance, and investment credit for allied and non-farm activities.

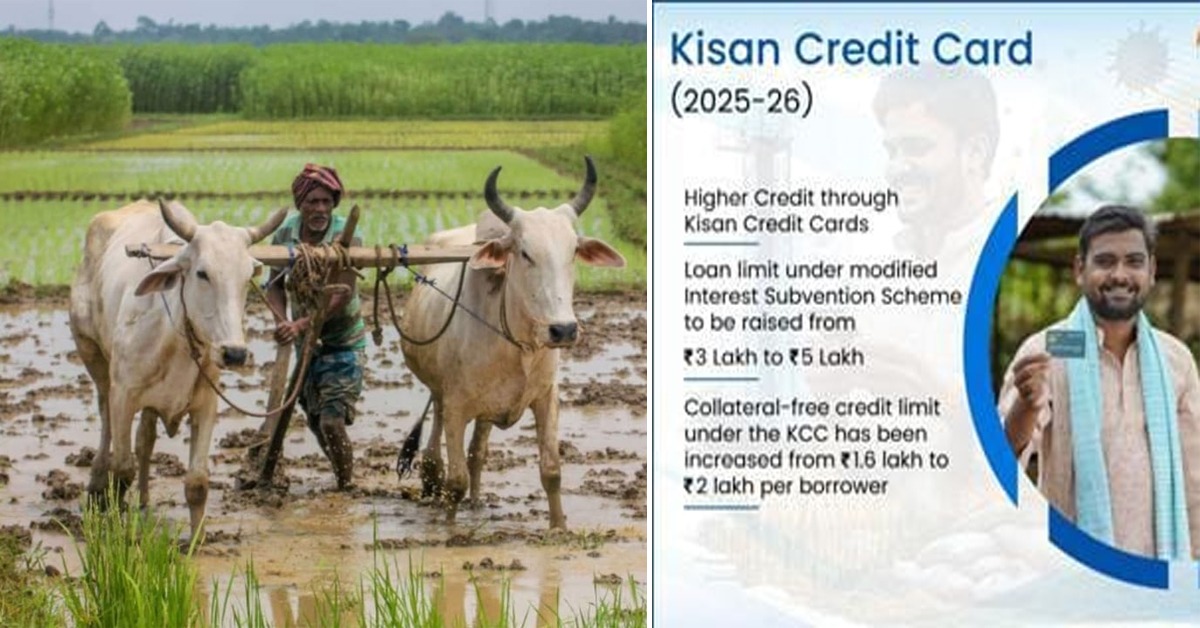

The Kisan Credit Card (KCC) Scheme, introduced in 1998, was designed to simplify and expedite farmers’ access to short-term institutional credit for crop production. It provides working capital and investment credit for allied activities and covers post-harvest and marketing expenses, thereby offering comprehensive financial support to enhance farm incomes. To further improve the affordability of credit under the KCC, the Government launched the Modified Interest Subvention Scheme (MISS) as a Central Sector Scheme in 2006–07. The scheme ensures farmers have access to credit at affordable rates through the Kisan Credit Card (KCC). The scheme also supports farmers in recovering from natural calamities and promotes timely loan repayment, thereby easing overall financial stress. Over time, it expanded to cover allied and non-farm activities, with the Revised KCC Scheme (2020) providing integrated, single-window credit support. The revised KCC offers a RuPay-enabled card with flexible withdrawals, digital payments, and one-time documentation, making access to credit simple and efficient. It covers cultivation, post-harvest needs, allied, and non-farm activities, and is implemented through commercial, regional rural, and cooperative banks to ensure broad outreach.

The Kisan Credit Card (KCC) Scheme covers a wide range of farmer categories to promote inclusive and equitable access to institutional credit. It extends coverage to: individual farmers and joint borrowers who are owner-cultivators,tenant farmers, oral lessees, and sharecroppers.In addition, the scheme also includes Self Help Groups (SHGs) and Joint Liability Groups (JLGs), including groups formed by tenant farmers and sharecroppers,thereby ensuring broader financial inclusion across diverse farming communities.

Access to affordable and timely institutional credit is central to sustaining agricultural livelihoods and strengthening rural economies. The Kisan Credit Card (KCC) Scheme has addressed this need by creating a reliable credit mechanism that supports cultivation, allied activities, and post-harvest requirements within a single, flexible framework. The progressive evolution of the scheme reflects a shift from transaction-based lending towards a more holistic approach that aligns credit availability with farmers’ production cycles and income flows.

Digital Blueprint for Ease of Doing Business

More than 7.72 crore Kisan Credit Cards (KCCs) are currently operational across the country, with an outstanding credit amounting to Rs. 10.2 lakh crore. This reflects the extensive reach of the KCC scheme in facilitating access to institutional credit for farmers and underscores its critical role in supporting agricultural and allied activities through affordable, timely financing.

Under the Kisan Credit Card (KCC) platform, a total of 457 banks has been onboarded, including 37 commercial banks,46 regional rural banks, and 374 cooperative banks. It indicates a diversified delivery architecture to ensure broad geographic coverage and inclusive access to institutional credit for farmers nationwide. Across these institutions, a total of 1,998.7 lakh kisan credit card applications have been processed, of which 631.5 lakh were through commercial banks, 337.2 lakh through regional rural banks, and 1030.0 lakh through cooperative banks. It reflects the broad institutional participation in the KCC implementation and highlights the central role of cooperative banks in extending agricultural credit, particularly at the grassroots level.

Recent reforms, including enhanced credit limits, expanded coverage to allied sectors, and digital integration through the Kisan Rin Portal, have significantly improved outreach, transparency, and governance. By enabling data-driven monitoring, expediting loan processing, and ensuring transparent claim settlement, these measures have strengthened the operational efficiency of agricultural credit delivery. In the context of increasing climate-related and market risks, the KCC scheme serves as a critical policy instrument to enhance financial resilience, promote the formalization of credit, and support sustainable agricultural growth, thereby contributing to inclusive rural development and long-term sectoral stability. Its continued strengthening will remain essential for advancing inclusive rural development and long-term agrarian stability.